Navigating the world of tax-saving investments can be overwhelming, especially when you’re trying to decide between Unit Linked Insurance Plans (ULIPs) and Equity Linked Savings Schemes (ELSS). While both are eligible for tax deductions under Section 80C, their structures, benefits, and associated risks vary significantly. Let’s break down these differences so you can make an informed choice.

What Is a ULIP?

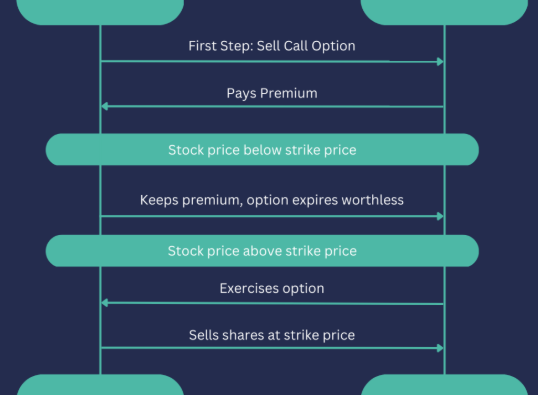

A ULIP is a versatile financial product that merges life insurance with investment. When you pay a premium, a part of it is allocated toward insurance coverage, and the rest is invested in funds—equity, debt, or a blend of both—based on your preference. One of the key traits of a ULIP is its five-year lock-in period, during which you cannot access the funds.

ULIPs offer the option to switch between investment types. This means if the market outlook shifts or your risk appetite changes, you can realign your portfolio accordingly without exiting the plan.

What Is ELSS?

ELSS is a mutual fund scheme that focuses on equity investments. It channels your money into stocks of companies listed on the stock exchange. The goal is to generate higher returns over time, though the exposure to equities makes it inherently riskier.

ELSS stands out for its short lock-in period of just three years, the lowest among investment instruments eligible under Section 80C. It’s a solid choice for investors willing to accept market volatility in exchange for the potential of superior returns.

How ULIP and ELSS Compare

1. Structure and Management

ULIPs are offered by insurance companies and combine life cover with investment options. ELSS funds are pure equity investments, managed by mutual fund companies.

2. Purpose

A ULIP addresses two goals at once: securing life insurance and building wealth. ELSS, on the other hand, is solely focused on long-term capital growth through equity markets.

3. Risk Level

ELSS tends to carry more risk due to its exposure to equities. In contrast, ULIPs allow investors to balance risk by diversifying between debt and equity, offering a more conservative route.

4. Performance Outlook

ELSS funds generally yield better long-term returns because of their exclusive equity exposure. ULIPs offer variable returns depending on how the invested funds are allocated.

5. Tax Rules

Both options allow for deductions up to ₹1.5 lakh under Section 80C. Post-redemption, ELSS is taxed similarly to other equity funds. ULIP proceeds are tax-exempt only if the annual premium is within ₹2.5 lakh; otherwise, gains may be taxable.

6. Withdrawal Flexibility

You can redeem ELSS units after three years, providing more liquidity. ULIPs restrict withdrawals for at least five years, making them less accessible in the short term.

7. Investment Control

ULIPs permit you to switch between fund types, which can help manage risk over time. ELSS investors do not have this flexibility, as the asset allocation remains consistent.

8. Charges and Fees

ULIPs usually involve higher fees due to insurance and fund management costs. ELSS typically carries a lower expense ratio, meaning less of your money goes toward administrative costs.

Final Thoughts

The better option depends on what you’re looking to achieve. If your priority is getting life insurance alongside investment growth—and you’re comfortable with a longer lock-in—then a ULIP might suit you. But if you’re focused purely on wealth creation and don’t mind riding market ups and downs, ELSS could be a smarter bet.

Both products serve valuable roles in a well-rounded financial plan. By understanding their features and aligning them with your own goals and risk tolerance, you can select the one that makes the most sense for your situation.